There is a cost you pay every single day you hold a mutual fund. It doesn’t appear as a deduction in your bank account. It doesn’t show up as a line item on your statement. It gets quietly subtracted from your fund’s value before the NAV is even published each evening.

It’s called the expense ratio — and over a long investment horizon, it can make a difference of lakhs in your final corpus.

Most investors know the term. Very few understand exactly how it works, who it goes to, and why even a difference of 0.5% deserves your serious attention.

What is the Expense Ratio?

The expense ratio is the annual fee that a mutual fund charges to manage your money. It covers the fund’s operating costs — the fund manager’s salary, administrative expenses, registrar fees, marketing costs, distributor commissions, and more. It is expressed as a percentage of the fund’s Average Daily Net Assets (ADNA).

If a fund has an expense ratio of 1.5% per year, it means ₹1.50 is charged annually for every ₹100 you have invested.

But here’s what makes it invisible: this charge is not deducted from your account directly. Instead, it is factored into the daily NAV calculation. The NAV you see published every day is already net of the expense ratio. You never see the deduction — you just receive slightly less growth than the fund’s gross returns.

What Goes Inside the Expense Ratio?

The expense ratio is not a single fee — it is a bundle of several costs rolled into one number:

Investment Management Fee: The largest component. This is what the AMC earns for the fund manager’s expertise and the research team’s work. Typically ranges from 0.50% to 1.25% depending on the fund type.

Administrative and Operational Costs: Includes registrar and transfer agent fees, audit fees, custodian charges, and fund accounting costs. These are relatively small but real.

Distribution and Commission Costs: If you invested through a distributor, broker, or bank, a portion of the expense ratio goes to them as trail commission — typically 0.50% to 1% annually. This is why the regular plan of any mutual fund has a higher expense ratio than its direct plan.

Marketing and Selling Expenses: AMCs spend on advertising, investor education, and outreach. These costs are also embedded here, within SEBI-prescribed limits.

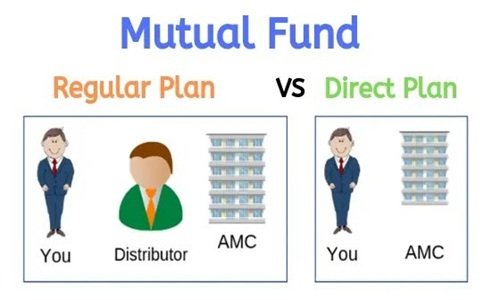

Regular Plan vs. Direct Plan: The Hidden Gap

This is the most important practical implication of understanding the expense ratio.

Every mutual fund in India offers two versions of the same scheme:

Regular Plan — bought through a distributor, bank, or broker. Higher expense ratio because it includes the distributor’s commission.

Direct Plan — bought directly from the AMC or through direct platforms. Lower expense ratio because no commission is paid to any intermediary.

The difference typically ranges from 0.5% to 1.5% per year depending on the fund category. On a ₹10 lakh investment over 20 years at 12% gross returns, that 1% annual difference in expense ratio can translate to a gap of over ₹30–35 lakhs in final corpus. Same fund. Same fund manager. Just a different plan.

This is not a small number. It is a compounding tax on your loyalty to convenience.

SEBI’s Expense Ratio Limits

SEBI regulates how much an AMC can charge as expense ratio. The limits are tiered based on the fund’s AUM (Assets Under Management) — larger funds are required to charge less, passing scale benefits to investors.

As a general reference, actively managed equity funds can charge up to 2.25% for smaller AUM slabs, with the limit reducing as AUM grows. Debt funds have lower caps. Index funds and ETFs, being passively managed, typically charge between 0.05% to 0.20% — a fraction of active fund costs.

You can always find the current Total Expense Ratio (TER) of any fund on the AMC’s website or on AMFI’s official portal. It is updated monthly.

Does a Lower Expense Ratio Always Mean a Better Fund?

Not automatically — but it is a significant factor. A fund charging 2% that consistently delivers 15% returns is better than a fund charging 0.5% that delivers 9%. What matters is net return to the investor, not gross performance.

However, research consistently shows that in most categories — especially large-cap equity and debt funds — actively managed funds rarely outperform their benchmark by enough to justify the higher expense ratio over the long term. This is a core argument for index funds in a diversified portfolio.

FAQs

Q1. Is the expense ratio charged even if the fund gives negative returns?

A: Yes. The expense ratio is charged regardless of whether the fund makes a profit or a loss. It is deducted from the NAV daily, irrespective of market conditions.

Q2. How do I check a fund’s expense ratio before investing?

A: Check the fund’s factsheet on the AMC website, its page on AMFI’s portal, or any major comparison platform like Morningstar India, Value Research, or MFCentral. Always compare the direct plan TER specifically.

Q3. Can the expense ratio change after I invest?

A: Yes. AMCs can revise expense ratios within SEBI’s prescribed limits. Any change is disclosed on the AMC’s website and communicated through regulatory filings. Monitor it periodically.

Q4. Is GST included in the expense ratio?

A: No. GST at 18% is charged over and above the expense ratio on the investment management fee component. This slightly increases the effective cost beyond the headline TER figure.

Q5. For a long-term SIP of 15–20 years, how much does 1% extra expense ratio actually cost?

A: On a monthly SIP of ₹10,000 over 20 years at 12% gross returns, a 1% higher expense ratio can reduce your final corpus by approximately ₹15–18 lakhs. The longer the horizon, the more damaging the difference due to compounding.