When people invest in mutual funds, most of the focus usually goes toward returns. Investors compare which fund gave 12%, which gave 15%, and which one performed best in the last five years. But many people ignore one small detail that quietly affects long-term wealth — the expense ratio.

This is where the difference between Direct Plans and Regular Plans becomes important.

At first glance, the difference may look tiny. In many cases, a Regular Plan may charge around 1% more annually than a Direct Plan. One percent may sound too small to matter. But over 20 years, that “small” difference can grow into lakhs of rupees.

That is the real power of compounding — and unfortunately, compounding also works against investors when costs are higher.

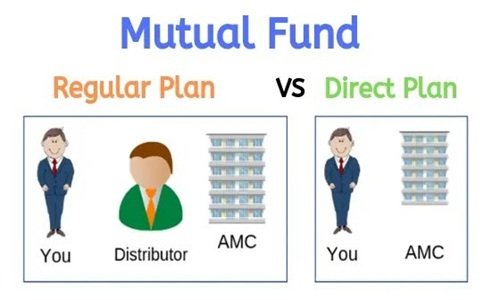

What Are Direct and Regular Mutual Fund Plans?

Mutual funds in India generally offer two types of plans:

Direct Plan

A Direct Plan is purchased directly from the mutual fund company without involving any distributor, broker, or agent. Since there is no commission paid to intermediaries, the expense ratio is lower.

This means investors keep a larger share of the returns.

Regular Plan

A Regular Plan is bought through an agent, bank, broker, or financial advisor. The mutual fund company pays commission to the distributor, and that cost is included in the expense ratio.

As a result, the investor earns slightly lower returns compared to the Direct Plan of the same fund.

The fund manager, portfolio, and investment strategy remain exactly the same. The only major difference is the cost.

Understanding the 1% Difference

Let us understand this with a simple example.

Suppose two investors invest ₹10,000 every month for 20 years.

- Investor A chooses a Direct Plan giving an average return of 12% annually.

- Investor B chooses a Regular Plan where expenses reduce the effective return to 11%.

The difference is only 1%.

But after 20 years, the gap becomes surprisingly large.

Approximate Results

- Direct Plan Corpus: Around ₹99 lakh

- Regular Plan Corpus: Around ₹87 lakh

Difference: Nearly ₹12 lakh

That extra ₹12 lakh did not come from investing more money. It came simply from saving 1% annually in costs.

Why Does This Happen?

The answer lies in compounding.

Every year, higher expenses reduce your returns slightly. In the next year, you earn returns on a smaller amount. Then the cycle repeats for decades.

Over time, even a tiny percentage difference starts creating a massive wealth gap.

This is why experienced investors often pay close attention to fees and costs instead of only chasing high returns.

Expense Ratio Explained Simply

The expense ratio is the annual fee charged by a mutual fund for managing your money.

It includes:

- Fund management charges

- Administrative costs

- Marketing expenses

- Distributor commissions

Direct Plans have lower expense ratios because distributor commissions are removed.

For example:

- Direct Plan Expense Ratio: 0.8%

- Regular Plan Expense Ratio: 1.8%

That extra 1% directly affects investor returns every single year.

Are Direct Plans Always Better?

Not necessarily for everyone.

Direct Plans are generally better for investors who:

- Understand mutual funds

- Can select funds independently

- Are comfortable using investment apps or AMC websites

- Do not need continuous advisory support

However, Regular Plans may still help some investors.

For example:

- Beginners who need guidance

- People uncomfortable with financial decisions

- Investors who prefer personal assistance

- Those needing tax and portfolio planning support

In such cases, the commission may act like a service fee for professional advice.

The key question is whether the advice received is worth the additional cost.

The Psychology of Small Numbers

One reason many investors ignore the Direct vs. Regular debate is because 1% feels insignificant.

People often think:

“What difference can 1% really make?”

But investing is a long-term game. In long durations, small percentages become powerful.

A 1% higher return every year for 20 years can create a dramatic difference in final wealth. The longer the investment horizon, the bigger the impact.

SIP Investors Feel the Difference More

Systematic Investment Plan (SIP) investors especially benefit from lower expenses because they invest regularly for many years.

Young investors starting SIPs in their 20s or early 30s can potentially save lakhs by choosing lower-cost investment options early.

Even retirement planning gets affected significantly by expense ratios.

Should You Switch From Regular to Direct?

Many investors today are gradually shifting from Regular Plans to Direct Plans because of growing awareness and easy online investing platforms.

However, before switching, investors should consider:

- Exit load charges

- Tax implications

- Whether they still need advisory support

- Portfolio review requirements

Blindly switching without understanding the full picture may not always be wise.

Final Thoughts

The difference between Direct and Regular Plans is one of the best examples of how small financial decisions shape long-term wealth.

A 1% cost difference may look harmless today, but over 20 years, it can mean losing several lakhs in potential wealth creation.

This does not mean Regular Plans are bad. Good financial advisors can add value through discipline, asset allocation, and long-term planning.

But investors should at least understand what they are paying for and how costs affect compounding.

In investing, returns matter. But costs matter too.

And sometimes, the smallest percentages create the biggest differences.

FAQs

Q1. What is the main difference between Direct and Regular Plans?

A: The main difference is cost. Direct Plans have lower expense ratios because there is no distributor commission, while Regular Plans include commission charges.

Q2. Do Direct Plans give higher returns?

A: Yes, generally Direct Plans provide slightly higher returns because of lower expenses.

Q3. Is a Direct Plan riskier than a Regular Plan?

A: No. Both invest in the same portfolio and carry the same market risk.

Q4. Can beginners invest in Direct Plans?

A: Yes, but beginners should first understand mutual funds properly before making independent investment decisions.

Q5. How much difference can 1% make in the long term?

A: Over 20 years, even a 1% difference can lead to several lakhs of difference because of compounding.

A: Q6. Can I switch from a Regular Plan to a Direct Plan?

A: Yes, investors can switch, but they should check tax implications and exit load charges before doing so.

Q7. Why do some people still choose Regular Plans?

A: Many investors prefer Regular Plans because they receive guidance, support, and financial planning assistance from advisors or distributors.